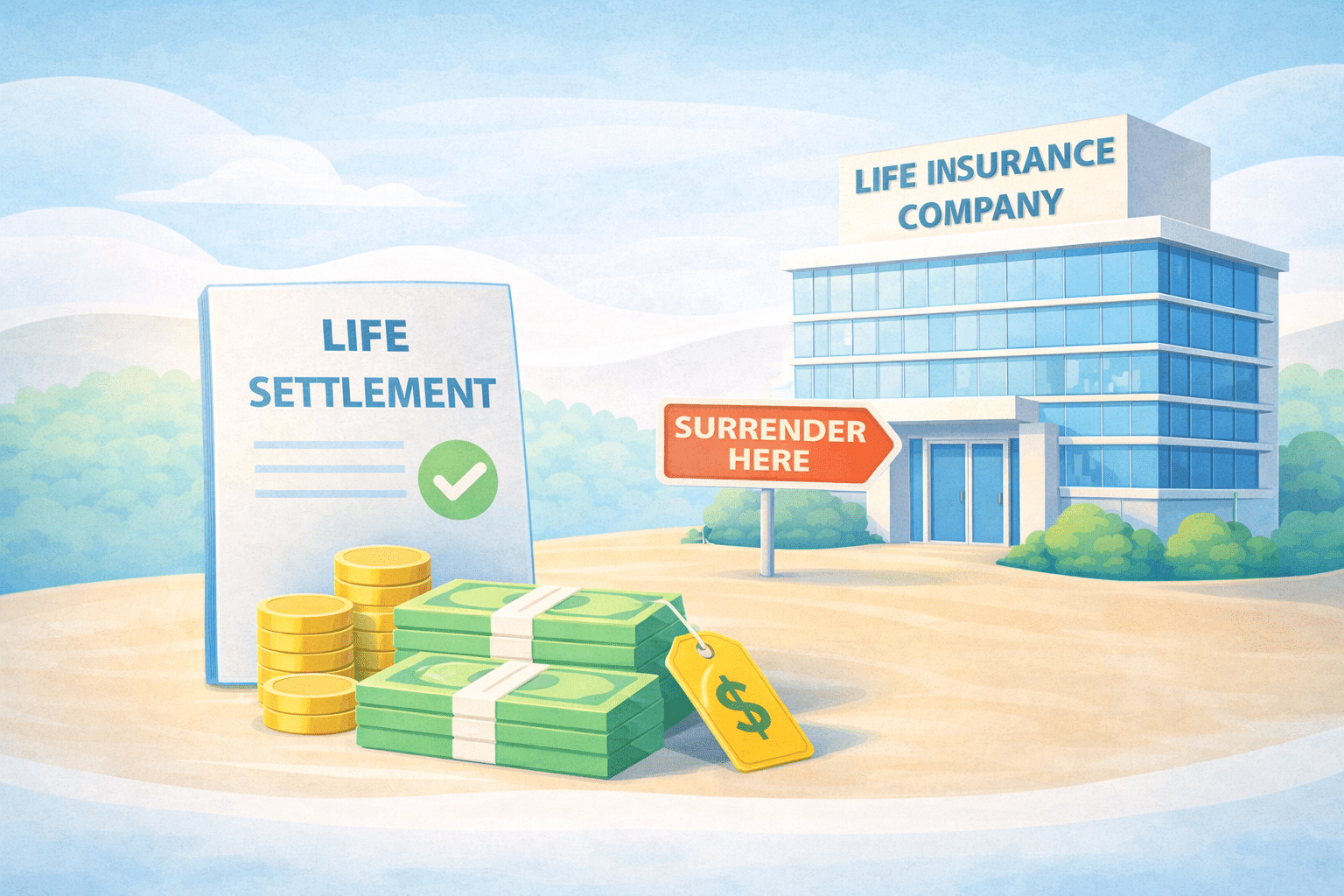

Life Settlement Definition

Why Sell To A Life Insurance Policy

The 7 Reasons Why To Sell A Life Insurance Policy in 2020

Life Insurance Coverage is No Longer Needed

Your Estate Tax Exemption Has Changed

Premiums Have Increased

Fund Your Retirement

Fund Long Term Care, Such As Assisted Living

Genworth offers a very user friendly and helpful Cost Of Living Survey that allows a user to enter their data to provide a general Cost Of Living for Long Term Care, based on 2018 data. This is very useful for seniors interested in learning and planning for Long Term Care. Calculate for yourself at Genworth