Universal life insurance is often purchased for its flexibility—the ability to adjust premiums, build cash value, and adapt coverage over time. But as years pass, many policyholders discover that flexibility can come at a cost. Premiums may rise, policy performance may fall short of expectations, or the policy may no longer fit current financial priorities.

When that happens, surrendering the policy often feels like the default solution.

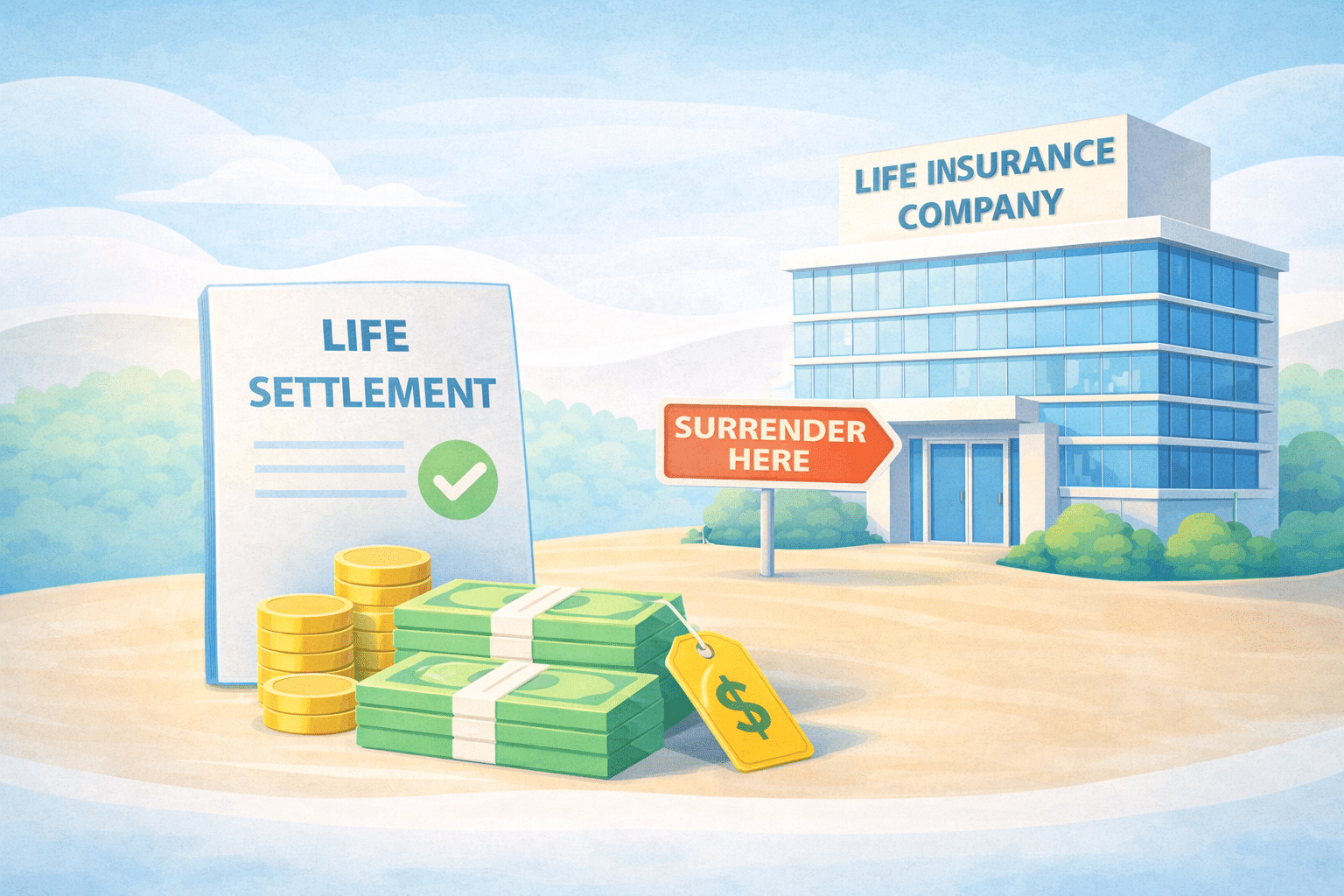

What many policyholders don’t realize is that surrender is usually the least favorable financial outcome. In many cases, a universal life insurance policy can instead be sold as a life settlement, allowing the policyholder to access market-based value rather than a carrier-determined surrender amount.

This article explains why surrendering is rarely the best first step, how universal life policies are evaluated in the life settlement market, and how working with an experienced life settlement broker can help policyholders pursue the strongest possible offers.

Why Universal Life Policies Are Often Surrendered Too Early

Universal life policies are complex. Over time, policyholders may encounter:

- Increasing cost-of-insurance charges

- Higher required premiums to keep the policy active

- Cash value erosion

- Policy performance that no longer aligns with original illustrations

When these issues arise, surrendering the policy can appear simple and final.

Why “Don’t Surrender” Matters

Surrendering a universal life policy may not always be the best financial option.

Selling the policy as a life settlement introduces a marketplace where third parties evaluate the policy’s future obligations and potential value. Because multiple buyers may assess the same policy differently, offers often exceed the cash surrender value—sometimes substantially.

When a policy is sold as a life settlement:

- The buyer assumes responsibility for future premiums

- The policyholder receives a lump-sum cash payment

- The policyholder no longer carries ongoing policy costs

For policies that are becoming financially inefficient, a life settlement can represent a materially better outcome than surrender.

Who Buys Universal Life Policies?

Universal life policies that qualify for a life settlement are typically purchased by institutional life settlement providers. These firms specialize in acquiring existing life insurance policies as long-term financial assets.

Well-known life settlement providers in this market include Coventry, these providers evaluate policies based on underwriting criteria, premium requirements, policy mechanics, and long-term sustainability.

The Role of a Life Settlement Broker

Because life settlement providers value policies differently, the way a policy is presented to the market can significantly affect the outcome.

This is where an independent life settlement broker plays a central role.

Life Policy Solutions works on behalf of policyholders to review universal life insurance policies and determine whether selling the policy as a life settlement—or, when applicable, a viatical settlement—is a viable option. Rather than representing a single buyer, a life settlement broker positions the policy across multiple qualified life settlement providers to encourage competitive review.

The objective is straightforward: ensure the policyholder understands all available options and pursue the highest possible life settlement offer, rather than defaulting to surrender or cancellation.

Life Settlement vs. Viatical Settlement for Universal Life Policies

In some cases, a universal life insurance policy may qualify for a viatical settlement instead of a life settlement, depending on medical eligibility.

- A life settlement is generally based on age, health profile, and policy characteristics

- A viatical settlement applies when a qualifying serious, or terminal illness is present and often results in higher offers

A proper evaluation determines which option applies. Reviewing both possibilities helps ensure that no potential value is overlooked.

Why Universal Life Policies Are Strong Candidates

Universal life policies are often attractive in the life settlement market because they offer structural flexibility. Features that can increase interest include:

- Adjustable premium designs

- Transparent funding and policy histories

- Modifiable death benefits

- Predictable long-term maintenance for providers

When evaluated correctly, these characteristics can translate into stronger demand and improved life settlement outcomes.

When Selling a Universal Life Policy Makes Sense

Exploring a life settlement or viatical settlement may be appropriate when:

- Premiums are rising or becoming difficult to justify

- The policy no longer aligns with long-term financial planning

- Cash value is underperforming

- Liquidity and flexibility have become priorities

Every situation is unique, but surrender should rarely be the first decision without understanding the policy’s market value.

A Smarter Alternative to Surrender

Universal life insurance policies are sophisticated financial instruments. Treating them as disposable assets through surrender often leaves meaningful value behind.

For policyholders willing to explore alternatives, selling a universal life policy as a life settlement—or, when applicable, a viatical settlement—offers a more informed and financially efficient path forward. Before surrendering a policy, understanding its potential value in the life settlement market can make all the difference.