When a family first begins planning for assisted living, the focus is almost always on care itself.

Finding the right community. Understanding what level of support is needed. Making sure the environment feels comfortable, safe, social, and appropriate not only for today, but potentially for years ahead.

But after the move happens and the first few months settle in, families often begin seeing assisted living differently.

The monthly cost is not always static. Care needs change. Medication support may increase. Mobility challenges may evolve. In some situations, memory care eventually becomes part of the picture.

And slowly, the financial side of care planning becomes more connected to the care itself.

Families begin asking practical questions:

- How do we preserve stability long-term?

- What happens if care needs increase later?

- How do we avoid burning through savings too aggressively early on?

- How do we maintain flexibility if circumstances change?

That is often when existing assets begin getting reviewed more carefully — including life insurance policies.

For many families, that policy has been sitting quietly in the background for years.

What they may not realize is that it could potentially become part of the assisted living care plan itself.

The Asset Many Families Overlook

Most people think of life insurance as something designed only for beneficiaries later on.

Because of that, policies are often ignored once retirement and long-term care planning begin.

Some families continue paying premiums without ever revisiting whether the policy still makes sense. Others surrender the policy back to the insurance company for a relatively small cash value simply because they assume those are the only available options.

But in some situations, the policy itself may hold substantially more value than the family realizes.

That value may potentially be used to help support:

- assisted living

- memory care

- home healthcare

- future care planning

- protecting savings for a spouse

- preserving long-term flexibility

Three Ways Life Insurance May Help Support Care

Once assisted living becomes part of the conversation, many families begin reviewing whether the policy includes any living benefits or other options that may help support care costs.

1. Accelerated Death Benefits (ADB Riders)

Many life insurance policies include provisions that allow the policyholder to access part of the death benefit while still alive under qualifying conditions.

Depending on the policy, this may apply in situations involving:

- chronic illness

- terminal illness

- cognitive decline

- inability to perform certain daily living activities

These benefits are often called:

- Accelerated Death Benefits

- Chronic Illness Riders

- Long-Term Care Riders

In some situations, these funds may help offset assisted living or long-term care expenses without requiring the policy to be sold.

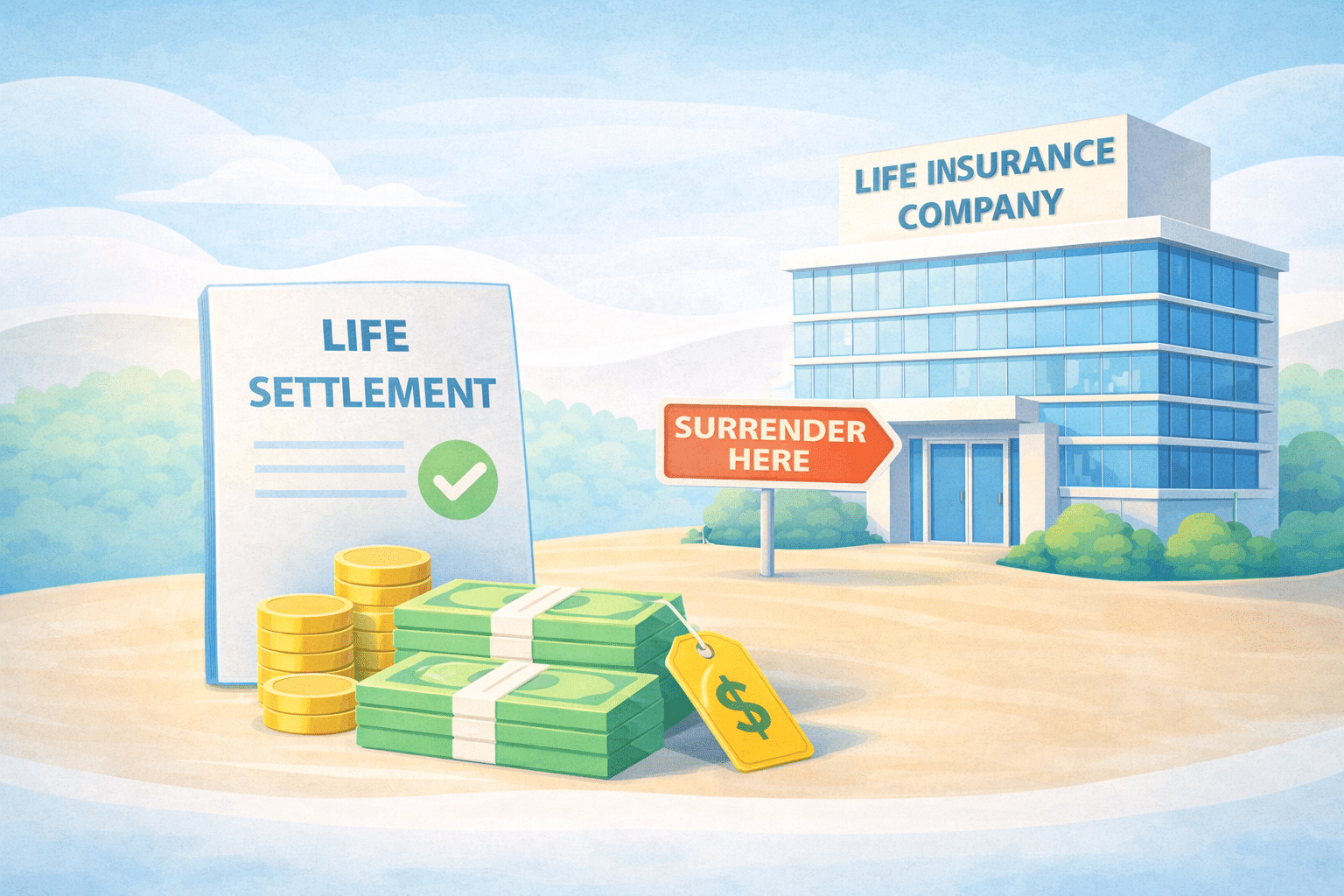

2. Life Settlements

If the policy does not contain meaningful living benefits — or if the available rider value is limited — some families begin exploring a life settlement instead.

A life settlement allows a qualifying life insurance policy to be sold for a lump sum cash payment.

For families already balancing rising assisted living costs with future care uncertainty, this option can completely change the care planning conversation.

In some situations, the proceeds may help:

- maintain a preferred assisted living community longer

- prepare for future memory care costs

- reduce pressure on retirement savings

- eliminate ongoing premium payments

- provide additional care flexibility moving forward

Many families discover life settlements only after assisted living planning has already begun.

Not because they were searching for one specifically — but because they started looking more carefully at what resources were already available.

3. Policy Loans and Withdrawals

Permanent life insurance policies such as Whole Life or Universal Life policies may also contain accumulated cash value.

Depending on the structure of the policy, families may be able to:

- withdraw part of the value

- borrow against the policy

- use the funds to help offset care-related costs

In some cases, this may provide temporary flexibility without requiring the policy itself to be sold.

Why Assisted Living Changes Financial Conversations

Assisted living planning often starts with immediate needs.

But over time, families naturally begin thinking farther ahead.

The conversation shifts from:

- What does care cost today?

to: - What happens if care needs become more involved later on?

- How do we preserve flexibility if circumstances change?

- How do we avoid creating unnecessary financial pressure five years from now?

These conversations become especially important when families begin realizing how closely future care decisions and long-term financial stability can become connected.

A senior may eventually require:

- additional daily assistance

- specialized mobility support

- memory care

- more advanced medical supervision

And because of that, families often begin thinking more carefully about how existing resources may best support care over time.

For some, the life insurance policy remains exactly where it belongs — untouched and preserved for the future.

For others, assisted living changes how the policy itself is viewed.

Instead of sitting quietly in the background, it may become part of the broader conversation surrounding care planning, stability, and preserving future options as needs evolve.

That does not mean every policy qualifies for a life settlement.

And it does not mean every family chooses to pursue one.

But understanding the option before surrendering a policy or allowing it to lapse can help families make more informed decisions while planning for long-term care.

Assisted Living Benefits from Planning

Assisted living planning is rarely just about the present moment. Families are often trying to make decisions that will still feel sustainable, supportive, and realistic years down the road as care needs continue evolving.

A life insurance policy can be an important asset during assisted living planning. In some situations, it may help a family begin care sooner, continue care longer, or adjust more comfortably as needs evolve over time. Having the right information and understanding the available options can help families feel more grounded and better prepared while navigating the financial path that often comes with assisted living in the years ahead.

Life Policy Solutions helps seniors and families explore life settlement options for assisted living, memory care, long-term care planning, and retirement-related healthcare expenses. Families can privately review whether an existing life insurance policy may qualify for a life settlement using the company’s free life settlement calculator, which requires no contact information to use.