Retirement is lasting longer — and costing more — than many seniors expected.

Healthcare expenses are rising. Inflation continues to pressure fixed incomes. And many retirees are looking for ways to strengthen retirement without draining savings or selling investments during uncertain markets.

At the same time, millions of seniors are still paying premiums on life insurance policies they may no longer need.

That is why more retirees are exploring life settlements.

A life settlement allows a senior to legally sell an existing life insurance policy for a lump sum cash payment — often significantly more than the policy’s surrender value.

For some retirees, it can turn an unused policy into immediate financial flexibility.

Why Seniors Reevaluate Life Insurance in Retirement

Life insurance is often purchased decades earlier to protect children, cover a mortgage, or replace income during working years.

But retirement changes things.

Children grow up. Homes get paid off. Financial priorities shift.

What once served as protection may eventually become:

- an expensive premium payment

- an underused asset

- a policy no longer needed

Rather than surrendering the policy back to the insurance company, some seniors discover the policy itself may have real market value.

A Hidden Retirement Asset

Many people do not realize life insurance policies can sometimes be sold.

Policies are considered personal property, and depending on age, health, policy type, and premium structure, institutional buyers may compete to purchase them.

That is especially true for:

- universal life policies

- whole life policies

- certain convertible term policies

For qualifying seniors, a life settlement can create immediate cash that can be used however they choose.

How Retirees Use Life Settlement Funds

Every situation is different, but seniors commonly use life settlement proceeds to:

- supplement retirement income

- pay healthcare expenses

- eliminate debt

- support a spouse

- build emergency reserves

- help family members

- improve overall retirement flexibility

For many retirees, the goal is simple: reduce financial pressure and gain more control over retirement decisions.

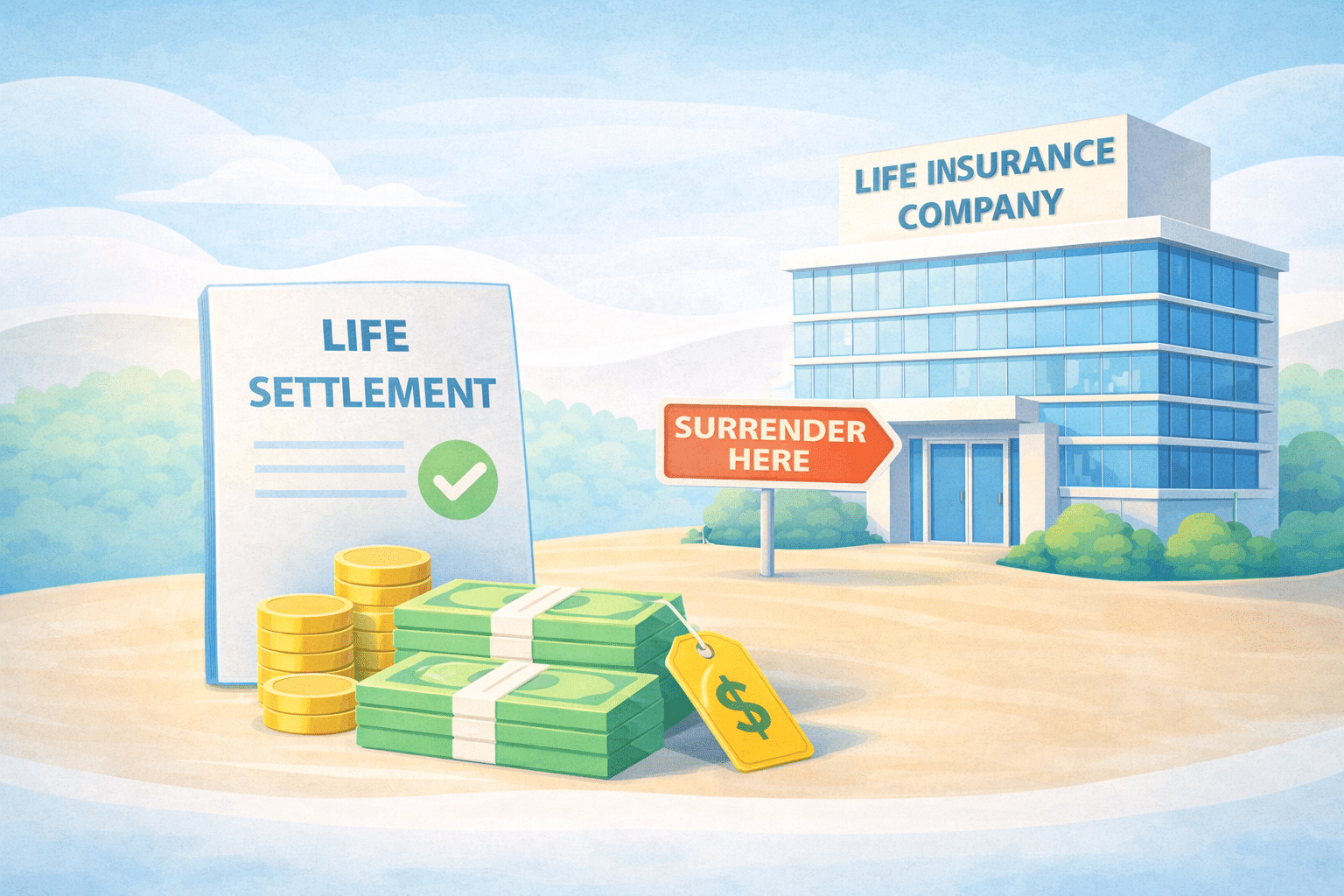

The Mistake Many Seniors Make

One of the biggest mistakes retirees make is allowing a policy to lapse or surrendering it without first understanding its potential market value.

In some cases, a life settlement may generate substantially more than the surrender value offered by the insurance company.

Unfortunately, many seniors are never told a secondary market for life insurance even exists.

Why the Type of Company Matters

Not all life settlement companies operate the same way.

Some life settlement companies are direct buyers that make one offer directly to the policy owner. You may have seen commercials advertising their services, these include Coventry Direct and Abacus Life. Direct Buyers offer a faster, more direct approach to the life settlement process, but there is potential for the policy owner to leave money on the table as the direct buyer is not competing against other buyers.

Life settlement brokers represents the policy owner in the sale process. A life settlement broker has the job to create competition among multiple institutional buyers through an auction marketplace. The goal of a life settlement broker is to use the competition to create increased life settlement value resulting in higher offers presented to the policy owner.

The difference of Direct Buyers vs Life Settlement Broker can matter financially, resulting in the amount your policy ultimately sells for.

Life Policy Solutions is a nationally recognized life settlement broker, helping seniors access competitive offers from multiple buyers rather than relying on a single valuation. In addition to creating a competitive marketplace for seniors to sell their policy, Life Policy Solutions offers industry leading guidance, knowledge, and transparency to policy owners.

Can Term Life Insurance Be Sold?

Sometimes, yes.

Many seniors assume term policies have no value, but certain convertible term policies may qualify for a life settlement if conversion rights remain active.

Timing matters, which is why reviewing a policy before surrendering it can be important.

A Growing Retirement Strategy

As retirement planning evolves, more seniors are beginning to view life insurance differently.

For some, an unwanted policy is no longer just a death benefit.

It may also represent a financial asset that can help strengthen retirement today.

Before surrendering a policy or letting it lapse, retirees should understand all available options and whether their policy may hold more value in the secondary market.

A life settlement may change your retirement planning today and for the future.

Life Policy Solutions offers a free Life Settlement Calculator that allows seniors to explore potential policy value privately with no contact information required.